Student loan forgiveness: what other options do you have if you don’t qualify for Biden’s new plan?

The expanding SAVE programme might not be the best choice for all borrowers, here’s a selection of what else is on offer.

The SAVE plan, announced late last summer, amended the terms of the Revised Pay As You Earn (REPAYE). The proposed regulations increase the amount of income protected from repayment from 150 percent of the Federal poverty guidelines to 225 percent. That level is roughly the equivalent of a $15 hourly wage based on the 2022 guidelines for a single borrower working full-time.

UPDATE: Our Administration just cancelled student debt for over 150,000 borrowers currently enrolled in the SAVE plan.

— The White House (@WhiteHouse) February 21, 2024

In total, our Administration has now approved nearly $138 billion in student debt cancellation for almost 3.9 million borrowers through various actions. pic.twitter.com/ftNjIwqGe9

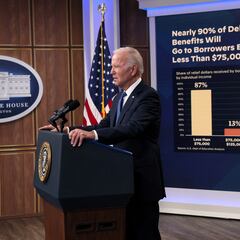

A single borrower earning less than $32,800 would have their monthly payments reduced to zero dollars. The same would be true for a borrower in a household of four with an annual income below $67,500. Under the most generous current income-driven repayment (IDR) plans the amounts are around $20,400 and just above $41,600 respectively. The thresholds will be higher in Hawaii and Alaska and those whose income exceeds them could see savings of at least $1,000 per year compared to other IDR plans.

Under the plan, the amount borrowers would be required to pay above the increased level of 225 percent will be half of the most generous IDR plan. Payments on loans borrowed for undergraduate studies will be reduced to just 5% of discretionary income. For those who have both undergraduate and graduate loans, the payment will be a weighted average of between 5 percent and 10 percent of their income based on the original principal balances.

Alternatives to SAVE plan

Income-driven repayment plans adjust your monthly payments based on your income and family size, making them more affordable. The government offers four income-driven repayment plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR).

This relief is for borrowers who paid on their student debt for 10 years and originally borrowed less than $12,000 and enrolled in the SAVE plan. This relief is a huge win for people who now have changed lives, but the Biden admin needs to keep building on this, and faster. https://t.co/ZGZqpdiJDx

— The Debt Collective 🟥 (@StrikeDebt) February 21, 2024

Related stories

Student-loan borrowers can take advantage of Public Service Loan Forgiveness (PSLF) programme. This programme forgives the remaining balance on your federal Direct Loans after you have made 120 qualifying payments while working full-time for a qualifying employer in public service or non-profit organisations. This provides the possibility for a borrower to have their debt cancelled in 10 to 20 years, respectively.

The White House also announced proposed changes to shorten the time for debt to be forgiven under IDR plans to just 10 years of payments, even if those payments are for zero dollars per month, in some cases. The proposal could also cut payments in half by raising the threshold for income protected from repayment in addtion to stopping interest from accumulating if monthly payments are made.